March CPI Report: Softer Inflation Print Calms Markets—for Now

The Consumer Price Index (CPI) report for March delivered a welcome surprise to financial markets Thursday morning, easing concerns of persistent inflation and reinforcing the case for a more patient Federal Reserve. While CPI is not the Fed’s preferred inflation gauge—that title belongs to the Personal Consumption Expenditures (PCE) Index—it remains the most politically and market-sensitive data point released each month. CPI reports have consistently driven significant equity volatility over the past year, often triggering sharp rallies or selloffs depending on whether inflation exceeded or missed expectations.

In fact, CPI days have become so impactful that they are easy to identify on index charts; large green or red candles often coincide with these releases. Despite the Fed's focus on PCE, CPI resonates more directly with consumers because it reflects price changes in the most visible categories—food, gasoline, shelter—and thus holds substantial sway over public sentiment and, by extension, political pressure. That’s part of why the market treats each CPI print as a potential inflection point.

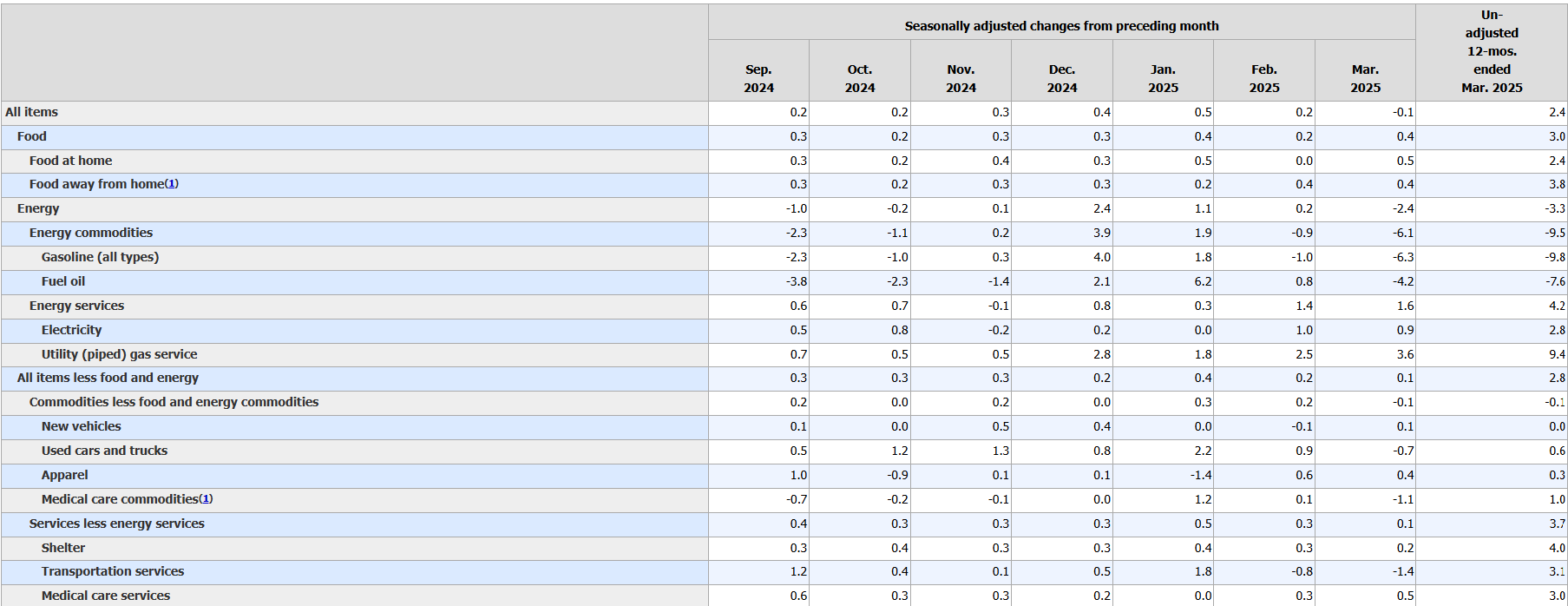

There are four key numbers in each CPI report that traders hone in on: headline CPI month-over-month (M/M), headline CPI year-over-year (Y/Y), core CPI M/M, and core CPI Y/Y. Headline figures include food and energy, which are volatile and influenced by global dynamics, while core figures strip out those elements to offer a cleaner read on underlying inflation pressures. The March report came in below expectations across all four metrics: headline CPI fell -0.1% M/M (vs. +0.1% expected) and rose 2.4% Y/Y (vs. 2.6% consensus), while core CPI rose just 0.1% M/M (vs. 0.3% expected) and 2.8% Y/Y (vs. 3.0%).

We would temper the enthusiasm around these results as most market participants are looking at the April and May readings as more reflective of the impact of tariffs on prices.

Heading into the release, investors were particularly nervous. Stagflation chatter has resurfaced in recent weeks as growth data softens while inflation metrics remain elevated. A hotter-than-expected CPI print would have amplified those concerns and cast doubt on the Fed’s ability to cut rates in 2025. Instead, today’s soft CPI gave markets a breather, reinforcing the narrative that price pressures may be easing just as growth begins to decelerate. The 2.8% core CPI Y/Y is now the lowest since March 2021, and the report’s overall tone was disinflationary.

That said, market participants were bracing for fireworks. Options market positioning ahead of the release implied a 1.5% move in the S&P 500—the most elevated implied volatility heading into a CPI report since March 2023. This level of hedging reflected deep uncertainty and set the stage for a sharp move regardless of the data’s direction. With CPI landing on the dovish side, equities are seeing a more muted but still positive reaction, and Treasury yields have come in slightly as Fed rate cut odds rise.

The structure of the CPI report is also important for interpreting market responses. It typically starts with headline CPI (both M/M and Y/Y), then details the biggest category movers—this month, energy fell sharply (-2.4% M/M) due to a 6.3% drop in gasoline, while food rose 0.4%. The core inflation section followed, highlighting modest gains in shelter (+0.3%) and owners’ equivalent rent (+0.4%), but declines in used cars, airfares, and insurance helped offset those pressures. Finally, the report wrapped with notable insights, including that the 12-month rise in core CPI was the slowest since March 2021.

For those looking to dig deeper, Table A in the CPI release breaks down granular price changes across more than 200 categories. Traders often use this detail to spot trends in sector-specific inflation, whether it's apparel, housing, or healthcare—data that can guide positioning in consumer discretionary, real estate, and healthcare equities.

In conclusion, March’s CPI report arrived as a much-needed source of stability in a market still digesting a chaotic trade policy environment. While not enough to lock in Fed rate cuts just yet, the soft print lowers the odds of further tightening and helps validate market expectations for easing later this year. With options markets primed for volatility, today’s cooler inflation read may offer a temporary reprieve—but traders should remain alert. CPI reports remain the single most powerful market catalyst month after month, and with inflation still above the Fed’s 2% target, each release continues to carry significant risk.

Senior Analyst and trader with 20+ years experience with in-depth market coverage, economic trends, industry research, stock analysis, and investment ideas.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet