Jefferies Misses as Deal Drought, Market Uncertainty Weigh; Signals Caution Ahead of Q1 Bank Earnings Season

Jefferies Financial Group kicked off the Q1 bank earnings season with disappointing results, missing expectations on both earnings and revenue. The firm reported fiscal Q1 EPS of $0.57, well below the Street’s $0.94 estimate, on revenue of $1.59 billion, also short of consensus at $1.86 billion. The shortfall was largely attributed to ongoing weakness in equity underwriting, reduced asset management returns, and subdued fixed income trading—pressures that management squarely blamed on U.S. policy uncertainty and geopolitical volatility. The stock fell 4% after hours, offering an early warning to investors ahead of earnings from Goldman SachsGBXC--, Morgan StanleyMS--, and JPMorganJPIN-- in mid-April.

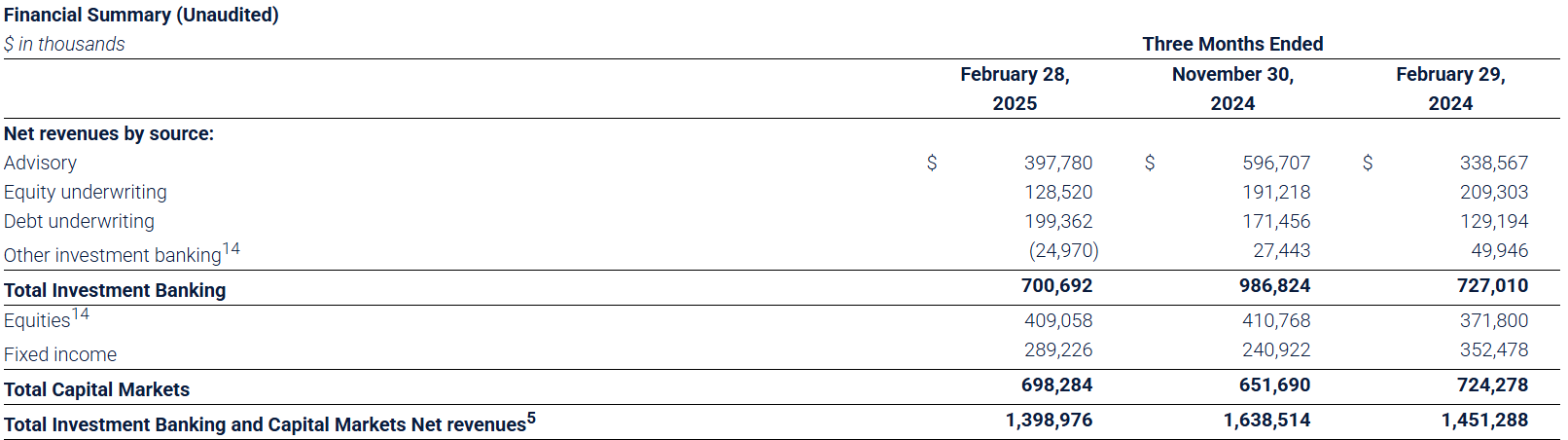

Investment banking revenue rose 7% year-over-year to $726 million, driven by a 17% gain in advisory revenue ($398 million) and a 54% jump in debt underwriting ($199 million). These gains, however, were overshadowed by a 39% plunge in equity underwriting to $129 million, reflecting a sharp slowdown in IPOs and secondary offerings. Capital markets revenue fell 4% to $698 million, dragged lower by an 18% year-over-year drop in fixed income trading to $289 million. While equities trading held up better, rising 10% to $409 million thanks to growth in prime services and electronic execution, the broader capital markets backdrop remained tough.

The asset management segment was a particular sore spot, with revenue falling 30% year-over-year to $192 million. Management fees and performance fees were solid, buoyed by strong 2024 fund performance, but overall investment return cratered in the face of a difficult macro environment—particularly for strategies with long equity exposure. Management said the investment environment was simply less conducive than the strong comparable period last year, leading to a sharp drop in this historically lumpy revenue stream.

Jefferies CEO Richard Handler and President Brian Friedman characterized the environment as “more challenging” due to geopolitical risks and U.S. trade policy, noting that visibility and deal confidence remain weak. Still, they maintained that Jefferies' advisory dialogue and transaction pipeline remain robust, with backlog building. “Its realization depends on confidence and visibility reemerging, which may be beginning,” Friedman said. The firm expressed confidence in its long-term strategy and reiterated a focus on risk discipline, client service, and market share gains across its platform.

Notably, Jefferies maintained its quarterly dividend at $0.40 per share and reported a drop in its effective tax rate to 9.4%, benefiting from the partial resolution of state and local tax issues. Book value per share rose to $49.48, with tangible book value per share climbing to $32.57, reflecting the firm’s continued focus on capital preservation despite near-term revenue headwinds.

With a 23% decline year-to-date in the stock and a growing divergence between advisory strength and capital markets weakness, Jefferies' results will be closely parsed by investors looking to gauge what’s ahead for the bulge-bracket banks. The company’s performance in fixed income—traditionally a strength for firms like JPMorgan and Morgan Stanley—was notably weak, adding to the growing sense that trading desks may not be the earnings buffer they were during more volatile periods.

Looking ahead, the main question for investors is whether Jefferies’ experience in Q1 reflects broader systemic challenges or idiosyncratic exposure. Deal dialogue remains active, but execution depends on improved visibility and more stable macro policy. The commentary about a “period of adjustment” suggests management expects improvement—just not imminently. With “Liberation Day” tariffs and evolving policy signals from Washington still on the horizon, investor sentiment may remain fragile until Q1 results across the sector provide more definitive direction.

Senior Analyst and trader with 20+ years experience with in-depth market coverage, economic trends, industry research, stock analysis, and investment ideas.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet