February PCE Report Shows Hotter-Than-Expected Inflation, Rekindling Market Jitters

The Federal Reserve’s preferred inflation gauge showed an unwelcome uptick in February, as hotter-than-expected core readings and upward revisions to recent trends rattled financial markets and sent U.S. equity futures toward session lows. The data came just days before the April 2 tariff deadline, and investors are already starting to see evidence that inflationary pressures tied to trade policy may be taking hold.

The core Personal Consumption Expenditures (PCE) price index—the Fed’s key measure of underlying inflation—rose 0.4% month-over-month in February, above the 0.3% consensus and up from January’s 0.3%. On a year-over-year basis, core PCE climbed to 2.8%, also ahead of expectations for 2.7% and up from 2.6% the prior month. That puts the annualized pace well above the Fed’s 2% target and signals renewed inflation stickiness after what had been a relatively benign start to 2024.

The all-items PCE index, which includes food and energy, increased 0.3% for the month, in line with expectations and flat versus January’s pace. Year-over-year, the headline figure held steady at 2.5%, matching consensus. But the disappointment came in the details, especially when looking at the more granular measures the Fed increasingly monitors.

One of the more troubling aspects of the report was the so-called “supercore” inflation reading—services prices excluding energy and housing. This measure jumped 0.4% month-over-month, up sharply from January’s 0.2%, and rose 3.34% year-over-year, accelerating from the prior 3.1%. That suggests sticky services inflation remains a stubborn issue, and it comes just as tariffs are set to push up goods prices in the months ahead.

Looking at trend dynamics, the six-month annualized rate for headline PCE now sits at 3.1%, while the three-month annualized pace has surged to 3.9%. These short- and medium-term accelerations will be closely watched by the Fed and argue against the idea that disinflation is continuing in a straight line.

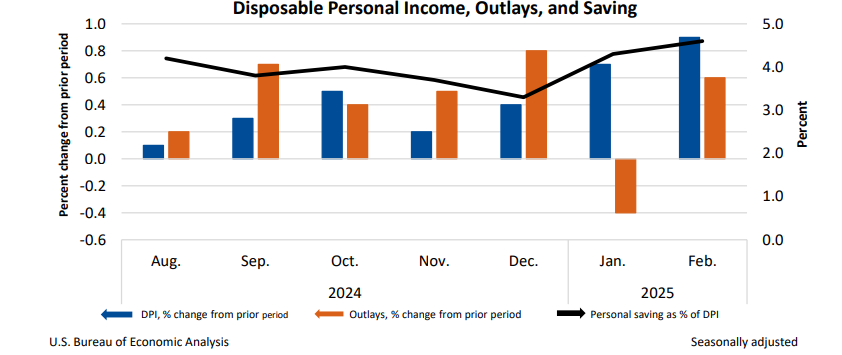

On the consumer side, the report was a mixed bag. Personal spending increased 0.4% month-over-month, shy of the 0.5% estimate, while real spending (adjusted for inflation) came in at just 0.1%. The spending rebound looks tepid when compared to January’s decline, and the miss adds weight to concerns that high prices and uncertainty may be crimping demand. On the other hand, personal income rose a robust 0.8% for the month, doubling the 0.4% estimate. That drove the personal saving rate up to 4.6% from 4.3%, suggesting households are choosing to bank more rather than spend amid rising prices and policy uncertainty.

The market reaction was swift. Equity futures, which were already under modest pressure overnight, slid further following the release. As of mid-morning, S&P 500 futures were down 0.4%, Nasdaq 100 futures had lost 0.6%, and Dow futures were off 0.3%. Treasury yields fell initially as risk assets weakened but may struggle to maintain a bid if inflation expectations become more entrenched.

The data also reignited hawkish rhetoric from some corners of the Fed-sphere. Former StST--. Louis Fed President James Bullard, speaking to Bloomberg shortly after the release, suggested a 50 basis point rate hike might be warranted if inflation remains elevated. While Bullard is no longer a voting member, his remarks reflect a broader concern that the market has perhaps moved too far in pricing in 2024 rate cuts, especially in a world where tariffs may structurally lift inflation.

Today’s numbers underscore a challenging setup for the Fed. While disinflation had been progressing, February’s figures suggest price pressures are not yet fully tamed—and the looming impact of Trump’s tariff plan could add another layer of complexity. The April 2 tariff announcement now looms even larger, with markets keen to assess not just the scope of the measures but their potential passthrough to consumer prices.

Bottom line: February’s PCE report does little to ease investor concerns. Core and supercore inflation are reaccelerating, near-term inflation momentum is building, and real spending is failing to impress. Add in geopolitical uncertainty and tariff-driven pricing pressures, and it’s clear the Fed may not have the latitude markets had hoped for. This isn’t the return to 2% inflation the Fed needs—it’s a warning shot that the final mile in the inflation fight could be the hardest.

Senior Analyst and trader with 20+ years experience with in-depth market coverage, economic trends, industry research, stock analysis, and investment ideas.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet