Dollar Tree Stock Pops on Family Dollar Sale, Mixed Q4 Earnings

Shares of Dollar TreeDLTR-- (DLTR) surged roughly 8% on Wednesday after the company announced a long-awaited deal to divest its struggling Family Dollar business and posted mixed fourth-quarter earnings. Investors cheered the $1.007 billion sale to private equity firms Brigade Capital Management and Macellum Capital Management, viewing the move as a crucial pivot in the company’s turnaround strategy.

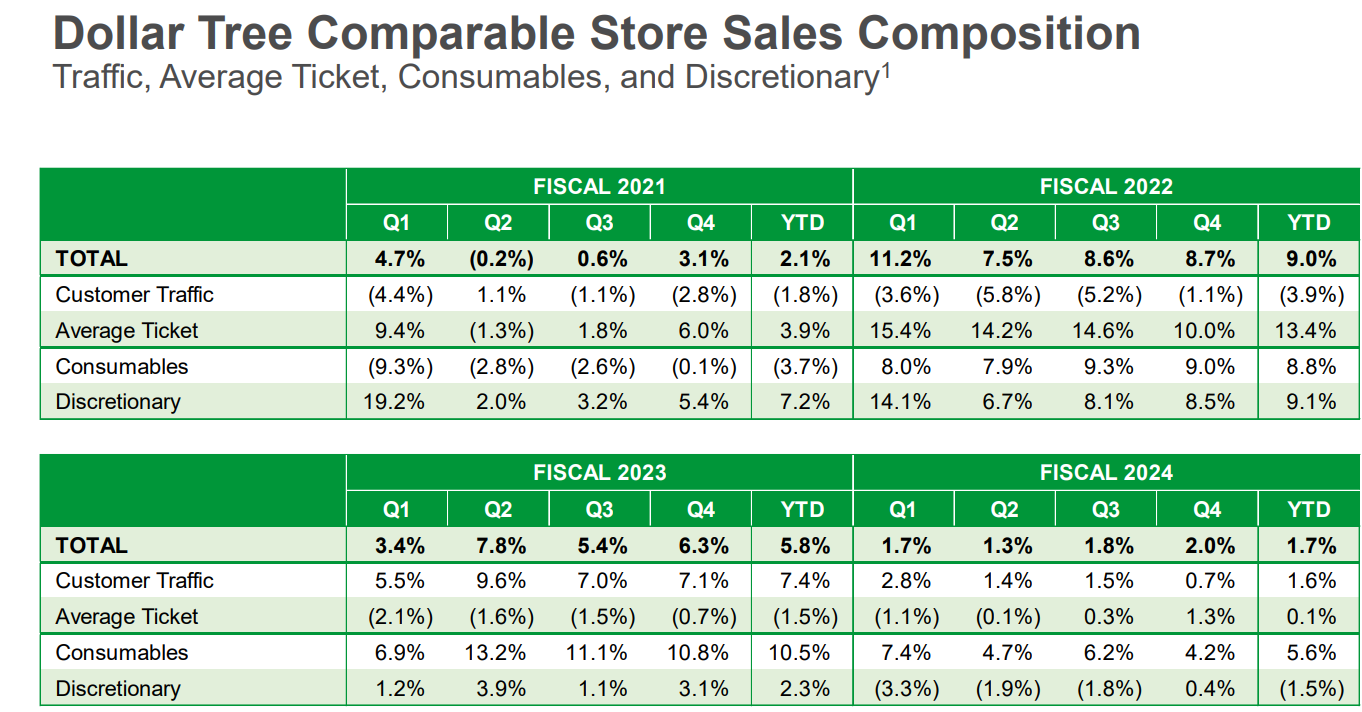

On the financial front, Dollar Tree reported adjusted Q4 earnings from continuing operations of $2.11 per share, falling short of the $2.21 consensus estimate and down from $2.55 a year ago. Net sales came in at $5.00 billion, a modest 0.7% increase from the prior year and slightly ahead of the $4.96 billion expected. Same-store sales rose 2.0%, supported by a 0.7% increase in traffic and a 1.3% gain in average ticket. These figures exclude Family Dollar, which has now been classified as discontinued operations.

Gross margin for the Dollar Tree segment contracted 130 basis points year over year to 37.6%, below the 38.7% consensus. The pressure stemmed from higher shrink, distribution, and markdown costs, partially offset by improved freight expenses. Notably, the quarter included a $25 million duty accrual related to an anti-dumping case. Operating income dropped 26.5% to $533.6 million, while adjusted operating margin fell 230 basis points to 12.6%.

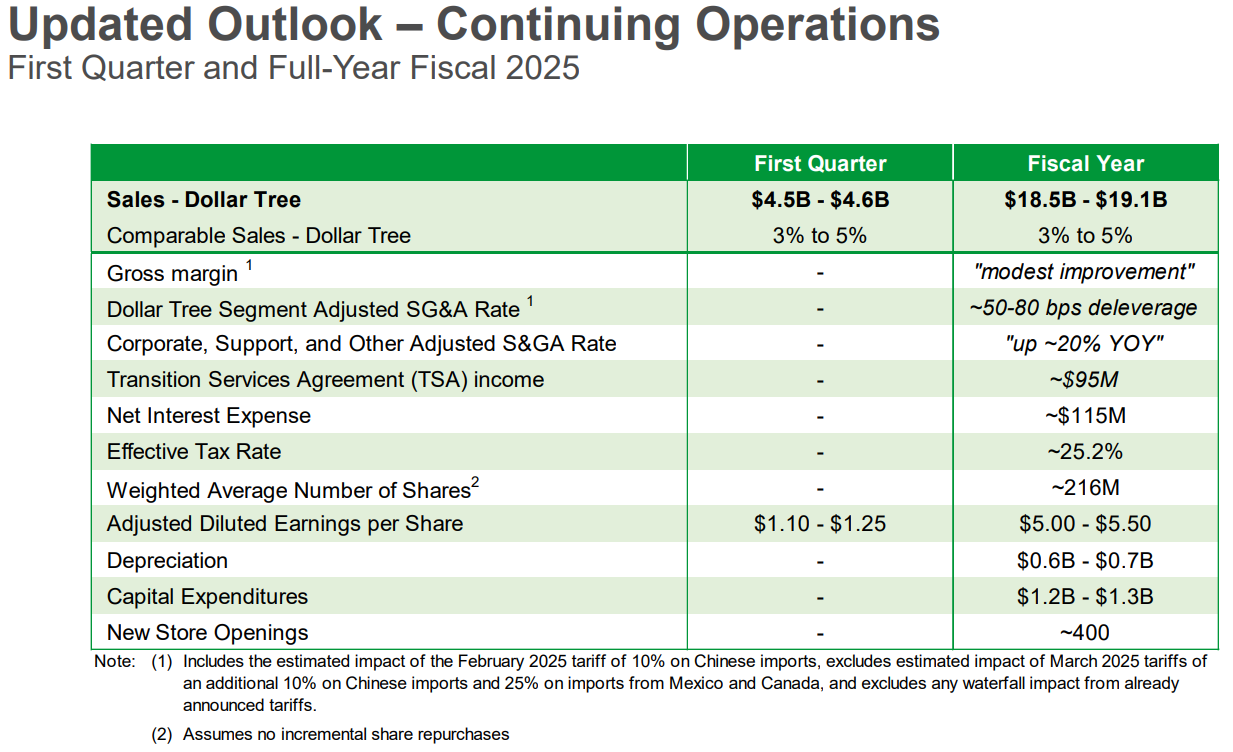

Looking ahead, Dollar Tree issued full-year fiscal 2025 guidance reflecting a leaner, more focused business. Net sales are expected to range from $18.5 billion to $19.1 billion, with comparable store sales growth projected between 3% and 5%. Adjusted EPS is forecasted between $5.00 and $5.50. The company noted a $0.30 to $0.35 earnings headwind from covering shared service costs for Family Dollar prior to the expected close of the transaction in Q2.

For Q1, the company guided to net sales of $4.5 billion to $4.6 billion and adjusted EPS between $1.10 and $1.25. These estimates incorporate the full burden of shared services expenses and no offsetting TSA reimbursement, which will only kick in after the deal closes.

The divestiture of Family Dollar, which Dollar Tree originally acquired for $9 billion in 2015, marks the end of a turbulent chapter. While the acquisition initially promised synergies, Family Dollar has long underperformed, weighed down by a challenging urban footprint, inflationary pressures, and operational inefficiencies. The company had already closed 1,000 stores earlier this year, signaling the unit's diminished viability. As part of the transaction, Family Dollar will remain headquartered in Chesapeake, Virginia, with Duncan MacNaughton appointed as Chairman.

Dollar Tree expects approximately $804 million in net proceeds from the sale and an estimated $350 million in tax benefits from associated losses. CEO Michael Creedon emphasized that the deal enables Dollar Tree to focus on expanding its core business and reinvesting in higher-growth areas. The company previously acquired leases from the bankrupt 99 Cents Only chain, signaling its intent to continue consolidating the discount retail space.

On tariffs, management cited $25 million in duties tied to an anti-dumping case but did not offer specific guidance on the broader impact of potential Trump administration tariffs expected to be detailed on April 2. However, given Dollar Tree’s heavy exposure to imported merchandise, tariff policy remains a key risk factor.

With the stock still trading at just 11x forward earnings and forming a multi-month base between $60 and $80 since last August, the breakup of the Family Dollar marriage may finally be clearing the runway for re-rating. For a name that’s spent years in retail purgatory, this quarter marks a turning point—less baggage, more optionality, and a story that investors may finally want to hear again.

Senior Analyst and trader with 20+ years experience with in-depth market coverage, economic trends, industry research, stock analysis, and investment ideas.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet