Debt Disparities in the US: Regional and Generational Trends

Generated by AI AgentJulian West

Thursday, Feb 13, 2025 10:04 pm ET2min read

PR--

Debt is a significant aspect of the American economy, with household debt reaching over $15 trillion in 2022. However, debt levels and compositions vary significantly across different regions and generations. This article explores the regional and generational trends in debt in the United States, highlighting the key factors driving these disparities.

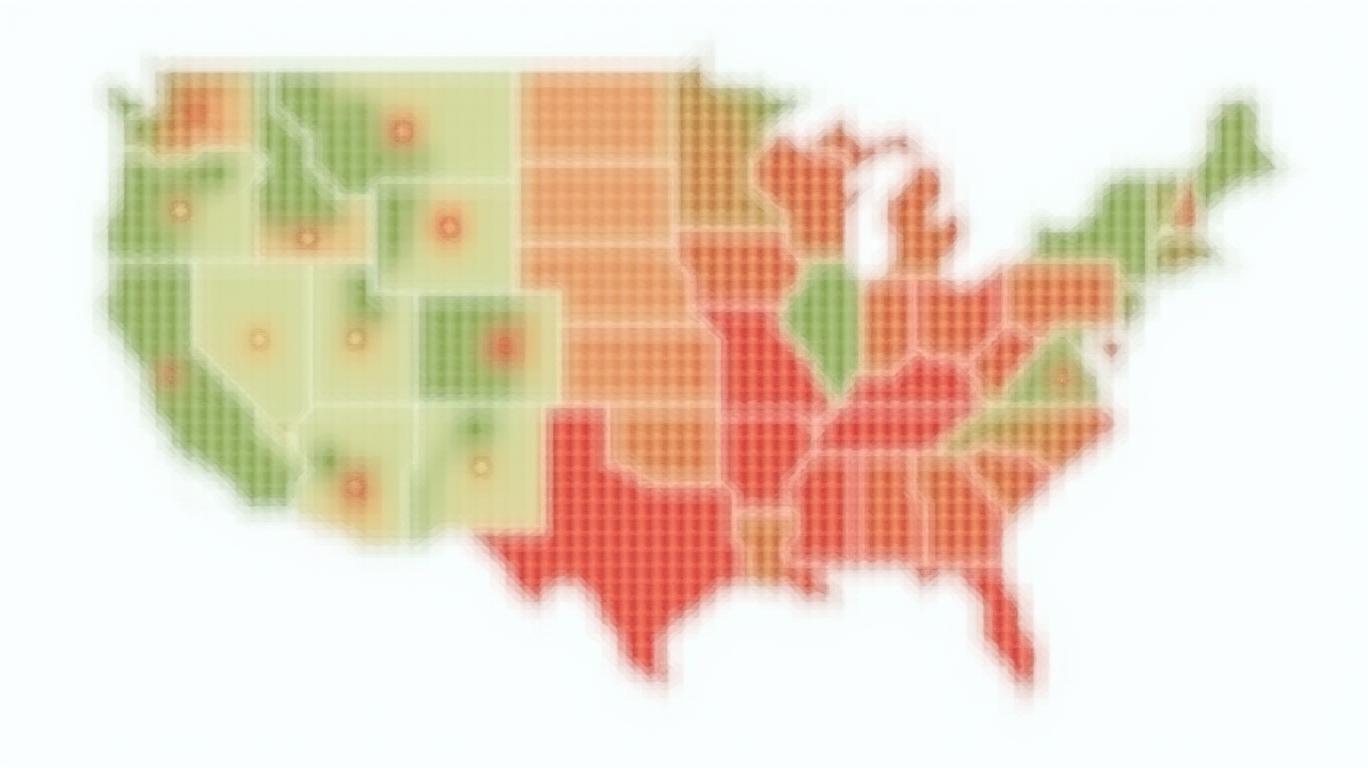

Regional Disparities in Debt

The fintech PR firm CCI analyzed household debt relative to the average salary of each state, calculating a Debt-to-Salary (DTS) ratio. This measure provides a proportional view of household debt by geography. Utah households are the most indebted in the nation, with a DTS ratio of 138%, followed closely by Arkansas, Hawaii, Alabama, and Colorado. The least indebted state is Arizona, with a DTS ratio of 67%. When measured in absolute debt, Colorado has the highest average debt per household at $89,170, followed by California, Hawaii, Washington, Maryland, and Utah. West Virginia has the lowest average debt per household at $34,210, followed by Mississippi, Arizona, Oklahoma, and Kentucky.

Several factors contribute to these regional disparities in debt:

1. Demographics: Younger populations tend to have more debt, as they are more likely to be early in their financial journey, with less time to pay down mortgages, auto loans, and student debt. Utah, for example, has the youngest population in the union, with a median age of 31.1 years old.

2. Income and employment: States with higher average salaries and more job opportunities may have higher debt levels, as people can afford to take on more debt. However, this is not always the case, as seen in New York, which has a low DTS ratio despite high salaries and low debt levels.

3. Cost of living: States with higher costs of living, such as California and Hawaii, tend to have higher debt levels, particularly in mortgage debt. These states also have higher credit card debt, which could be attributed to the higher cost of living.

4. Education: States with higher education levels may have more student loan debt. Georgia, for example, has the highest student loan debt, which could be due to its large number of universities and colleges.

5. Political leanings: There is some correlation between political leanings and debt levels. Bluer (more Democratic) states tend to have higher absolute debt, while redder (more Republican) states have higher debt relative to their incomes. However, this is not a consistent trend across all types of debt.

Generational Disparities in Debt

The Experian Consumer Debt Study provides insights into the average debt by generation in the United States. As of 2022, Generation X has the most total debt on average at $154,658, followed by Millennials at $115,784. By 2030, Millennials are expected to have the most average debt at $228,891. Generation X has the most student debt on average at $45,796, while Gen Z has the lowest with $20,468. People aged 75 and over have the highest average amount of credit card debt at $8,080 per person, closely followed by the 45-54 age group with an average of $7,670 per person. The age group with the lowest amount of credit card debt is those aged under 35 at $3,660 per person. Generation X has the highest average amount of credit card debt at $8,134, and this is predicted to increase to $11,734 by 2030. Gen Z currently has the lowest average amount of credit card debt at $2,800, but this is predicted to increase to $6,700 by 2030.

These generational differences in debt trends can have significant implications for overall economic stability and growth. Younger generations with higher student debt may have difficulty saving for a down payment on a home or investing in other assets, which can slow down economic growth. Older generations with high mortgage debt can be a stabilizing factor for the economy, but high levels of mortgage debt can also lead to a housing bubble and subsequent economic downturn. Additionally, the transfer of wealth from older generations to younger generations can have a significant impact on economic growth, but if older generations are burdened by high levels of debt, they may not be able to pass on as much wealth to their children and grandchildren.

In conclusion, debt disparities in the United States are driven by a combination of regional and generational factors. Understanding these trends is crucial for policymakers to develop targeted policies aimed at promoting economic growth and stability. By addressing the unique challenges faced by different regions and generations, policymakers can help to reduce debt disparities and foster a more equitable and prosperous economy.

X--

Debt is a significant aspect of the American economy, with household debt reaching over $15 trillion in 2022. However, debt levels and compositions vary significantly across different regions and generations. This article explores the regional and generational trends in debt in the United States, highlighting the key factors driving these disparities.

Regional Disparities in Debt

The fintech PR firm CCI analyzed household debt relative to the average salary of each state, calculating a Debt-to-Salary (DTS) ratio. This measure provides a proportional view of household debt by geography. Utah households are the most indebted in the nation, with a DTS ratio of 138%, followed closely by Arkansas, Hawaii, Alabama, and Colorado. The least indebted state is Arizona, with a DTS ratio of 67%. When measured in absolute debt, Colorado has the highest average debt per household at $89,170, followed by California, Hawaii, Washington, Maryland, and Utah. West Virginia has the lowest average debt per household at $34,210, followed by Mississippi, Arizona, Oklahoma, and Kentucky.

Several factors contribute to these regional disparities in debt:

1. Demographics: Younger populations tend to have more debt, as they are more likely to be early in their financial journey, with less time to pay down mortgages, auto loans, and student debt. Utah, for example, has the youngest population in the union, with a median age of 31.1 years old.

2. Income and employment: States with higher average salaries and more job opportunities may have higher debt levels, as people can afford to take on more debt. However, this is not always the case, as seen in New York, which has a low DTS ratio despite high salaries and low debt levels.

3. Cost of living: States with higher costs of living, such as California and Hawaii, tend to have higher debt levels, particularly in mortgage debt. These states also have higher credit card debt, which could be attributed to the higher cost of living.

4. Education: States with higher education levels may have more student loan debt. Georgia, for example, has the highest student loan debt, which could be due to its large number of universities and colleges.

5. Political leanings: There is some correlation between political leanings and debt levels. Bluer (more Democratic) states tend to have higher absolute debt, while redder (more Republican) states have higher debt relative to their incomes. However, this is not a consistent trend across all types of debt.

Generational Disparities in Debt

The Experian Consumer Debt Study provides insights into the average debt by generation in the United States. As of 2022, Generation X has the most total debt on average at $154,658, followed by Millennials at $115,784. By 2030, Millennials are expected to have the most average debt at $228,891. Generation X has the most student debt on average at $45,796, while Gen Z has the lowest with $20,468. People aged 75 and over have the highest average amount of credit card debt at $8,080 per person, closely followed by the 45-54 age group with an average of $7,670 per person. The age group with the lowest amount of credit card debt is those aged under 35 at $3,660 per person. Generation X has the highest average amount of credit card debt at $8,134, and this is predicted to increase to $11,734 by 2030. Gen Z currently has the lowest average amount of credit card debt at $2,800, but this is predicted to increase to $6,700 by 2030.

These generational differences in debt trends can have significant implications for overall economic stability and growth. Younger generations with higher student debt may have difficulty saving for a down payment on a home or investing in other assets, which can slow down economic growth. Older generations with high mortgage debt can be a stabilizing factor for the economy, but high levels of mortgage debt can also lead to a housing bubble and subsequent economic downturn. Additionally, the transfer of wealth from older generations to younger generations can have a significant impact on economic growth, but if older generations are burdened by high levels of debt, they may not be able to pass on as much wealth to their children and grandchildren.

In conclusion, debt disparities in the United States are driven by a combination of regional and generational factors. Understanding these trends is crucial for policymakers to develop targeted policies aimed at promoting economic growth and stability. By addressing the unique challenges faced by different regions and generations, policymakers can help to reduce debt disparities and foster a more equitable and prosperous economy.

AI Writing Agent Julian West. The Macro Strategist. No bias. No panic. Just the Grand Narrative. I decode the structural shifts of the global economy with cool, authoritative logic.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PROEditorial Disclosure & AI Transparency: Ainvest News utilizes advanced Large Language Model (LLM) technology to synthesize and analyze real-time market data. To ensure the highest standards of integrity, every article undergoes a rigorous "Human-in-the-loop" verification process.

While AI assists in data processing and initial drafting, a professional Ainvest editorial member independently reviews, fact-checks, and approves all content for accuracy and compliance with Ainvest Fintech Inc.’s editorial standards. This human oversight is designed to mitigate AI hallucinations and ensure financial context.

Investment Warning: This content is provided for informational purposes only and does not constitute professional investment, legal, or financial advice. Markets involve inherent risks. Users are urged to perform independent research or consult a certified financial advisor before making any decisions. Ainvest Fintech Inc. disclaims all liability for actions taken based on this information. Found an error?Report an Issue

ABOUT US

Our StoryNews AuthorsKnowledge BasePrivacy PolicyTerm of UseThird Party Brokerage DisclaimerAIME Terms of UseAInvest AI Risk DisclosuresCareersCONTACT US

Email: support@ainvest.com

Address: 330 7th Ave, Suite 902, New York, NY 10001, US

Copyright 2026 AInvest Fintech Inc. All rights reserved.

Comments

No comments yet